Wal-Mart (WMT) Dividend Stock Analysis

It's been over a year since I last looked at Wal-Mart (WMT) and I like what I see. I actually missed picking up some shares yesterday by $0.01. The joys of setting limit orders. I wanted to revisit this dividend champion discount retailer. Wal-mart closed trading on Wednesday, June 12th at $74.84.

Company Background (sourced from Yahoo! Finance):

Wal-Mart Stores, Inc. operates retail stores in various formats worldwide. The company operates in three segments: Walmart U.S., Walmart International, and Sam's Club. It operates retail stores, restaurants, discount stores, supermarkets, supercenters, hypermarkets, warehouse clubs, apparel stores, Sam’s Clubs, neighborhood markets, and other small formats, as well as walmart.com; and samsclub.com. The company’s stores offer meat, produce, deli, bakery, dairy, frozen foods, alcoholic and nonalcoholic beverages, and floral and dry grocery; health and beauty aids, baby products, household chemicals, paper goods, and pet supplies; and electronics, toys, cameras and supplies, photo processing services, cellular phones, cellular service plan contracts and prepaid service, movies, music, video games, and books. Its stores also provide stationery, automotive accessories, hardware and paint, sporting goods, fabrics and crafts, and seasonal merchandise; pharmacy and optical services, and over-the-counter drugs; shoes, jewelry, accessories, and apparel for women, girls, men, boys, and infants; and home furnishings, housewares and small appliances, bedding, home décor, outdoor living, and horticulture products. In addition, the company’s stores offer tobacco, tools and power equipment, office supplies, office and home furniture, grills, gardening products, toys, seasonal items, mattresses, and small appliances; and wireless, software, video games, movies, and music products, as well as operate gasoline stations, and tire and battery centers. Further, it operates banks that provide consumer financing programs; and offers financial services and related products, including money orders, prepaid cards, wire transfers, check cashing, and bill payment. As of June 3, 2013, the company operated approximately 10,800 stores under 69 banners in 27 countries and e-commerce Websites in 10 countries.

DCF Valuation:

Analysts expect Wal-mart to grow earnings 9.29% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter. Running these numbers through a two stage DCF analysis with a 10% discount rate yields a fair value price of $102.91. This means the shares are trading at a 27.3% discount to the DCF.

Graham Number:

With a current book value per share of $21.28 and TTM EPS of $5.08, the Graham Number is calculated to be $49.32. Currently Wal-mart is trading for a 51.8% premium to the Graham Number.

Average High Dividend Yield:

Wal-mart's average high dividend yield for the past 5 years is 2.65% and for the past 10 years is 2.13%. This gives target prices of $70.99 and $88.30 respectively based on the current annual dividend of $1.88. I think the 5 year average is more representative going forward and it will probably creep up higher as well. Wal-mart is currently trading at a 5.4% premium to the average high dividend yield valuation.

Average Low PE Ratio:

Wal-mart's average low PE ratio for the past 5 years is 11.98 and for the past 10 years is 14.94. This corresponds to a price per share of $63.51 and $79.16 respectively based off the analyst estimate of $5.30 per share for fiscal year 2014. WMT's low P/E ratio has been coming down since early in the 2000's due to the overvaluation back then as well as slowing of the growth. A 12-15 P/E ratio seems about right for Wal-mart so I'm using the average of the 2 for my target price. This works out to a 13.46 P/E ratio giving a price point of $71.34. Wal-mart is currently trading at a 4.9% premium to this price.

Average Low P/S Ratio:

Wal-mart's average low PS ratio for the past 5 years is 0.42 and for the past 10 years is 0.52. This corresponds to a price per share of $61.47 and $76.22 respectively based off the analyst estimate for revenue growth from FY 2013 to FY 2014. Currently, their current PS ratio is 0.53 on a trailing twelve months basis. Both ratios are relatively close so I'll use the average of the 2 again. This corresponds to a P/S ratio of 0.47 with a target price of $68.85. Wal-mart is currently trading at a 8.7% premium to this price.

Dividend Discount Model:

For the DDM, I assumed that Wal-mart will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 14.63%. After that I assumed they can continue to raise dividends for 3 years at 75% of 15% or 10.97% and in perpetuity at 3.50%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, Wal-mart is worth $52.55, meaning it's overvalued by 42.4%.

PE Ratios:

Wal-mart's trailing PE is 14.73 and it's forward PE is 12.86. The PE3 based on the average earnings for the last 3 years is 16.03. I like to see the PE3 be less than 15 which WMT is currently over by a bit. Compared to it's industry, Wal-mart seems to be undervalued versus COST (23.66) and TGT (16.31). All industry comparisons are on a TTM basis. Wal-mart's PEG for the next 5 years is currently at 1.53 while COST is at 1.79 and TGT is at 1.45. Based on the PEG ratio, Wal-mart undervalued versus COST and overvalued versus TGT. A lower PEG ratio is better because you're paying more less for the growth of the company.

Fundamentals:

Wal-mart's gross margins for FY 2012 and FY 2013 were 26.8% and 26.7% respectively. They have averaged a 25.6% gross profit margin since 2004 with a low of 24.0% in FY 2004. Their net income margin for the same years were 3.7% and 3.8%. Since 2004 their net income margin has averaged 3.6% with a low of 3.3% in FY 2009. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. Wal-mart is under both of my typical margin ranges; however, each industry is different and allows for different margins, retail is a notoriously low margin business. How is WMT doing compared to it's industry? For FY 2013, Wal-mart captured 95.4% of the gross margin for the industry and 115.2% of the net income margin. Being the world's largest retailer allows them to turn more of their sales into profits thanks to their efficient and large distribution network.

Share Buyback:

Wal-mart's shares outstanding have been decreasing the last 10 years. Since FY 2004, they've purchased 23.8% of their shares outstanding for an average annualized decrease of 2.7%. Looking at the amount spent on share buybacks, management increased the buyback program in FY 2010 and have kept it elevated since. Buybacks are great as long as they are purchasing shares at a value price point, otherwise they are reducing shareholder value through the buyback program. Looking at the historical data, the increased buyback program coincides with better value prices available in the market. By repurchasing shares, Wal-mart is able to increase EPS and management can return cash to shareholders this way by increasing the ownership stake of the company for all the outstanding shares.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Wal-mart is a dividend champion with 39 consecutive years of dividend increases. They have increased the dividend at a 18.24%, 15.82%, 14.63%, and 17.97% rate for the last 1,3,5, and 10 year periods. Nothing wrong with those levels as they will quickly juice the lower starting yield. The most recent increase was over 18%. Their payout ratio based off EPS has increased since FY 2004 which has allowed the dividend to increase faster than EPS have grown. I expect it to track closer to EPS growth going forward. Since FY 2004 the payout ratio has increased from 17.4% to 31.7% and has averaged 26.3% over that time.

Wal-mart's free cash flow has been great since FY 2003 growing at a 14.9% annualized rate. Their free cash flow payout ratio has averaged only 53.3% since FY 2004, which is higher than the payout based on earnings. Annual total shareholder return when accounting for buybacks plus dividends has averaged 146.5% of FCF since FY 2004 so it will have to come down or management will have to continue taking on debt to finance either the dividend, buybacks or capex.

Return on Equity and Return on Capital Invested:

Wal-mart's ROE has averaged 21.3% since 2004 and has been in a general uptrend ending FY 2013 at a 23.3% level. Their ROCI has averaged a 13.8% rate since 2004 and like their ROE has been increasing, ending FY 2013 at 15.1%. I don't necessarily look for any absolute values, rather I like to see stable to increasing levels over the long term because it shows the consistency that management is able to invest in growing the business.

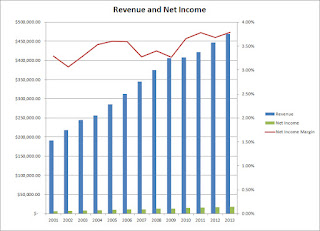

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Wal-mart has done on that front. Their revenue growth since 2003 has been solid with a 6.73% annual increase and their net income has been growing at a 8.25% rate. Since their net income has been growing faster than revenue, their net income margin has increased from 3.3% to 3.8% between FY 2003 and FY 2013. Over that time, Wal-mart hasn't had a decline in either revenue or net income which very few companies can say after the brutal economy between 2008-2012.

Forecast:

The chart shows the historical high and low prices since 2001 and the forecast based on the average PE ratios and the expected EPS values. I have also included a forecast based off a PE ratio that is only 75% of the average low PE ratio. I like to the look to buy at the 75% Low PE price or lower to provide for a large margin of safety, although this price doesn't usually come around very often. In the case of Wal-mart, the target low PE is 13.46 and the 0.75 * PE is 10.09. This corresponds to an entry price of $79.61 based off the expected earnings for FY 2014 of $5.30, with a 75% target price of $47.63. Currently Wal-mart is trading at a $27.21 premium to the 75% low PE target price and a $4.77 discount to the average PE price. If you believe the analyst estimates are pretty close, then Wal-mart is trading on the lower end of it's typical range but it's not at bargain basement levels.

Conclusion:

The average of all the valuation models gives a target entry price of $69.33 which means that Wal-mart is currently trading at a 8.0% premium to the target entry price. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and Graham Number valuations are removed and the new average is $65.93. Wal-mart is trading at a 13.5% premium to this price as well.

Assuming that Wal-mart can grow their earnings and dividends at the rates that I assumed, you're looking at solid returns over the next 10 years. In 2024, EPS would be $9.53 and slapping an average PE of 15.02 gives a price of $143.12. Over the next 10 years you'd also receive $38.93 in dividends for a total return of 243.3% which is good for a 9.3% annualized rate if you purchase at the current price. If you purchase at my target entry price of $69.33, your projected 10 year total return jumps to 262.58% for an annualized return of 10.14%.

I have a very small position in Wal-mart in my Roth IRA and I'm interested in starting a position in my taxable account. I feel that the continued growth of Wal-mart as a business will still be at a high level as they expand into the emerging market economies which will be a big driver of growth. Management has already shown a commitment to raising the dividend year in and year out so the dividend growth should follow. I actually almost started the position yesterday but my limit order missed by exactly $0.01. I wasn't going heavy with this position and still don't plan to based on the current price levels. If there's a dip down to the low $70's or even below $70 then I'll try and scoop up as much as I reasonably can.

To check out more reports check out my Stock Analysis page.

What do you think about Wal-mart as a DG investment at today's prices? How do you think the long-term dividend growth prospects are?

Company Background (sourced from Yahoo! Finance):

Wal-Mart Stores, Inc. operates retail stores in various formats worldwide. The company operates in three segments: Walmart U.S., Walmart International, and Sam's Club. It operates retail stores, restaurants, discount stores, supermarkets, supercenters, hypermarkets, warehouse clubs, apparel stores, Sam’s Clubs, neighborhood markets, and other small formats, as well as walmart.com; and samsclub.com. The company’s stores offer meat, produce, deli, bakery, dairy, frozen foods, alcoholic and nonalcoholic beverages, and floral and dry grocery; health and beauty aids, baby products, household chemicals, paper goods, and pet supplies; and electronics, toys, cameras and supplies, photo processing services, cellular phones, cellular service plan contracts and prepaid service, movies, music, video games, and books. Its stores also provide stationery, automotive accessories, hardware and paint, sporting goods, fabrics and crafts, and seasonal merchandise; pharmacy and optical services, and over-the-counter drugs; shoes, jewelry, accessories, and apparel for women, girls, men, boys, and infants; and home furnishings, housewares and small appliances, bedding, home décor, outdoor living, and horticulture products. In addition, the company’s stores offer tobacco, tools and power equipment, office supplies, office and home furniture, grills, gardening products, toys, seasonal items, mattresses, and small appliances; and wireless, software, video games, movies, and music products, as well as operate gasoline stations, and tire and battery centers. Further, it operates banks that provide consumer financing programs; and offers financial services and related products, including money orders, prepaid cards, wire transfers, check cashing, and bill payment. As of June 3, 2013, the company operated approximately 10,800 stores under 69 banners in 27 countries and e-commerce Websites in 10 countries.

DCF Valuation:

Analysts expect Wal-mart to grow earnings 9.29% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter. Running these numbers through a two stage DCF analysis with a 10% discount rate yields a fair value price of $102.91. This means the shares are trading at a 27.3% discount to the DCF.

Graham Number:

With a current book value per share of $21.28 and TTM EPS of $5.08, the Graham Number is calculated to be $49.32. Currently Wal-mart is trading for a 51.8% premium to the Graham Number.

Average High Dividend Yield:

Wal-mart's average high dividend yield for the past 5 years is 2.65% and for the past 10 years is 2.13%. This gives target prices of $70.99 and $88.30 respectively based on the current annual dividend of $1.88. I think the 5 year average is more representative going forward and it will probably creep up higher as well. Wal-mart is currently trading at a 5.4% premium to the average high dividend yield valuation.

Wal-mart's average low PE ratio for the past 5 years is 11.98 and for the past 10 years is 14.94. This corresponds to a price per share of $63.51 and $79.16 respectively based off the analyst estimate of $5.30 per share for fiscal year 2014. WMT's low P/E ratio has been coming down since early in the 2000's due to the overvaluation back then as well as slowing of the growth. A 12-15 P/E ratio seems about right for Wal-mart so I'm using the average of the 2 for my target price. This works out to a 13.46 P/E ratio giving a price point of $71.34. Wal-mart is currently trading at a 4.9% premium to this price.

Average Low P/S Ratio:

Wal-mart's average low PS ratio for the past 5 years is 0.42 and for the past 10 years is 0.52. This corresponds to a price per share of $61.47 and $76.22 respectively based off the analyst estimate for revenue growth from FY 2013 to FY 2014. Currently, their current PS ratio is 0.53 on a trailing twelve months basis. Both ratios are relatively close so I'll use the average of the 2 again. This corresponds to a P/S ratio of 0.47 with a target price of $68.85. Wal-mart is currently trading at a 8.7% premium to this price.

Dividend Discount Model:

For the DDM, I assumed that Wal-mart will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 14.63%. After that I assumed they can continue to raise dividends for 3 years at 75% of 15% or 10.97% and in perpetuity at 3.50%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, Wal-mart is worth $52.55, meaning it's overvalued by 42.4%.

PE Ratios:

Wal-mart's trailing PE is 14.73 and it's forward PE is 12.86. The PE3 based on the average earnings for the last 3 years is 16.03. I like to see the PE3 be less than 15 which WMT is currently over by a bit. Compared to it's industry, Wal-mart seems to be undervalued versus COST (23.66) and TGT (16.31). All industry comparisons are on a TTM basis. Wal-mart's PEG for the next 5 years is currently at 1.53 while COST is at 1.79 and TGT is at 1.45. Based on the PEG ratio, Wal-mart undervalued versus COST and overvalued versus TGT. A lower PEG ratio is better because you're paying more less for the growth of the company.

Fundamentals:

Wal-mart's gross margins for FY 2012 and FY 2013 were 26.8% and 26.7% respectively. They have averaged a 25.6% gross profit margin since 2004 with a low of 24.0% in FY 2004. Their net income margin for the same years were 3.7% and 3.8%. Since 2004 their net income margin has averaged 3.6% with a low of 3.3% in FY 2009. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. Wal-mart is under both of my typical margin ranges; however, each industry is different and allows for different margins, retail is a notoriously low margin business. How is WMT doing compared to it's industry? For FY 2013, Wal-mart captured 95.4% of the gross margin for the industry and 115.2% of the net income margin. Being the world's largest retailer allows them to turn more of their sales into profits thanks to their efficient and large distribution network.

Share Buyback:

Wal-mart's shares outstanding have been decreasing the last 10 years. Since FY 2004, they've purchased 23.8% of their shares outstanding for an average annualized decrease of 2.7%. Looking at the amount spent on share buybacks, management increased the buyback program in FY 2010 and have kept it elevated since. Buybacks are great as long as they are purchasing shares at a value price point, otherwise they are reducing shareholder value through the buyback program. Looking at the historical data, the increased buyback program coincides with better value prices available in the market. By repurchasing shares, Wal-mart is able to increase EPS and management can return cash to shareholders this way by increasing the ownership stake of the company for all the outstanding shares.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Wal-mart is a dividend champion with 39 consecutive years of dividend increases. They have increased the dividend at a 18.24%, 15.82%, 14.63%, and 17.97% rate for the last 1,3,5, and 10 year periods. Nothing wrong with those levels as they will quickly juice the lower starting yield. The most recent increase was over 18%. Their payout ratio based off EPS has increased since FY 2004 which has allowed the dividend to increase faster than EPS have grown. I expect it to track closer to EPS growth going forward. Since FY 2004 the payout ratio has increased from 17.4% to 31.7% and has averaged 26.3% over that time.

Wal-mart's free cash flow has been great since FY 2003 growing at a 14.9% annualized rate. Their free cash flow payout ratio has averaged only 53.3% since FY 2004, which is higher than the payout based on earnings. Annual total shareholder return when accounting for buybacks plus dividends has averaged 146.5% of FCF since FY 2004 so it will have to come down or management will have to continue taking on debt to finance either the dividend, buybacks or capex.

Return on Equity and Return on Capital Invested:

Wal-mart's ROE has averaged 21.3% since 2004 and has been in a general uptrend ending FY 2013 at a 23.3% level. Their ROCI has averaged a 13.8% rate since 2004 and like their ROE has been increasing, ending FY 2013 at 15.1%. I don't necessarily look for any absolute values, rather I like to see stable to increasing levels over the long term because it shows the consistency that management is able to invest in growing the business.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Wal-mart has done on that front. Their revenue growth since 2003 has been solid with a 6.73% annual increase and their net income has been growing at a 8.25% rate. Since their net income has been growing faster than revenue, their net income margin has increased from 3.3% to 3.8% between FY 2003 and FY 2013. Over that time, Wal-mart hasn't had a decline in either revenue or net income which very few companies can say after the brutal economy between 2008-2012.

Forecast:

Conclusion:

The average of all the valuation models gives a target entry price of $69.33 which means that Wal-mart is currently trading at a 8.0% premium to the target entry price. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and Graham Number valuations are removed and the new average is $65.93. Wal-mart is trading at a 13.5% premium to this price as well.

Assuming that Wal-mart can grow their earnings and dividends at the rates that I assumed, you're looking at solid returns over the next 10 years. In 2024, EPS would be $9.53 and slapping an average PE of 15.02 gives a price of $143.12. Over the next 10 years you'd also receive $38.93 in dividends for a total return of 243.3% which is good for a 9.3% annualized rate if you purchase at the current price. If you purchase at my target entry price of $69.33, your projected 10 year total return jumps to 262.58% for an annualized return of 10.14%.

I have a very small position in Wal-mart in my Roth IRA and I'm interested in starting a position in my taxable account. I feel that the continued growth of Wal-mart as a business will still be at a high level as they expand into the emerging market economies which will be a big driver of growth. Management has already shown a commitment to raising the dividend year in and year out so the dividend growth should follow. I actually almost started the position yesterday but my limit order missed by exactly $0.01. I wasn't going heavy with this position and still don't plan to based on the current price levels. If there's a dip down to the low $70's or even below $70 then I'll try and scoop up as much as I reasonably can.

To check out more reports check out my Stock Analysis page.

What do you think about Wal-mart as a DG investment at today's prices? How do you think the long-term dividend growth prospects are?

I thought about buying some WMT but never pulled the trigger. That was a few years ago and never thought about it again until today. I am not sure how I feel about them at the moment at todays prices. The numbers look good but I don't think I have anythng I would sell in order to scoop some shares of WalMart. How many share are you looking at getting this go around if you get some?

ReplyDeleteThomas,

DeleteI started a very small position in my ROTH in 2011 on the Mexican bribery scandal and got a great price on it. Unfortunately I don't think we'll be seeing those prices again anytime soon. I feel that WMT is one of the better options in the current market as far as being set up for good total returns going forward. I just wish the starting yield was higher.

At current prices I'm not really looking to load up that much, but if it gets close to $70 or under then I'll be picking up a good chunk. I've been leaning towards smaller purchases in the $1,500-1,800 range with the purchases I've been making because great value just isn't available in the market so I'm sticking with super high quality at reasonable prices. So somewhere in the 20-25 share range for WMT.

Thanks for stopping by!

I have wanted to buy WMT for a long time, but the stock never hits a point where the starting yield is high enough for me.

ReplyDeleteMyFIJ,

DeleteThe low starting yield is negative to owning WMT, although the DG is great. It's one of those situations where I think the quality is just too good to pass up. Not one year of negative revenue or net income growth since FY 2001. Considering that covers 2 pretty major economic troughs, that's impressive to me. I wish I could have picked up more during the Mexico bribery scandal, but just didn't have the cash available.

Thanks for stopping by!

Just selected WMT as 1 of the 6 stocks that could continue to surge in 2013 ;-)

ReplyDeleteThe stock is behind the stock market right now and I think it shouldn't be ignored. It will definitely continues to pay great dividend in the next 10 years.

Dividend Guy,

DeleteI noticed that and I have to say I agree. If only we could get a dip to give a 3.00% starting yield, although that might not be in the future. Who knows? Certainly not me, I've been expecting a pullback since February and all we've done is add over 1,000 more points to the DJIA. The quality and growth is still there so I decided to go on and pick up some more shares.

Thanks for stopping by!

I like the business, I can't get my head around the low starting yield for the investment case, around 3% I'd certainly consider it, but its a little less than where I'd like it to be. If I looked at similar targets in the large cap dividend space like McDonalds and Cola that are much closer to 3% starting yield, I'd be more comfortable placing my money there. I think you'll also likely do better than a 10% total return for both of these over the medium term.

ReplyDeleteIntegrator,

DeleteThat seems to be the main concern with WMT and was something that kind of drew me away from it as well. I wanted some more exposure to WMT because there's still plenty left in the tank for growth of the company as well as the dividend. While MCD and KO are also great companies, I can't really justify allocating more to either presently because they're both currently overweight in my portfolio. Although all 3 are great companies and think all 3 will provide greater than 10% total returns going forward.

Thanks for stopping by!